This page is part of the English restoration corpus. It keeps noindex during review and does not replace existing high-ID archive shells.

【CPC Market】High Inventory + Weak Demand: Will Calcined Petroleum Coke Prices Struggle to Improve?

Market Overview

On April 8, the average price of calcined petroleum coke was 3,360 yuan/ton, unchanged from the previous working day. Currently, the low-sulfur calcined petroleum coke market is weak and stable in price, with high inventories at production enterprises and weak demand. Downstream enterprises have few inquiries. Prices in the medium-to-high sulfur calcined petroleum coke market remain stable. Although raw petroleum coke prices have slightly rebounded, downstream buyers of medium-to-high sulfur calcined petroleum coke are pressing for lower prices. As a result, calcined petroleum coke producers are mainly shipping at stable prices, and price increases are lacking momentum.

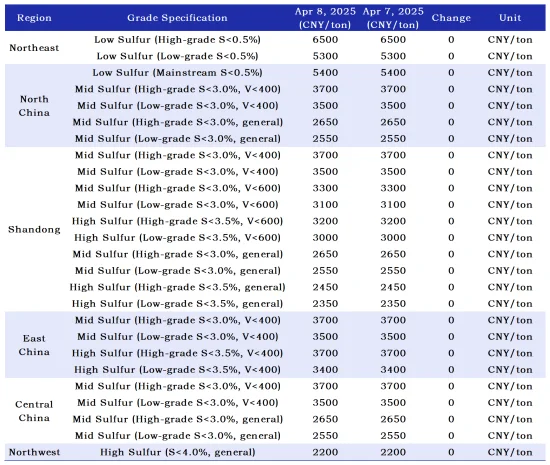

Main Regional Market Transaction Prices

Market Prices

1. Low-sulfur calcined petroleum coke (using Jinxi, Jinzhou petroleum coke as raw materials): Mainstream transaction prices are 5,200–5,500 yuan/ton.

2. Low-sulfur calcined petroleum coke (using Fushun petroleum coke as raw material): Ex-factory mainstream transaction prices are 6,200–6,500 yuan/ton.

3. Low-sulfur calcined petroleum coke (using Liaohe, Binzhou CNOOC petroleum coke as raw materials): Mainstream transaction prices are 5,300–5,800 yuan/ton.

4. Medium-to-high sulfur calcined petroleum coke (3.0% sulfur, no requirement for trace elements): Previous ex-factory mainstream contract prices were 2,550–2,650 yuan/ton (cash); currently negotiated prices are still 2,550–2,650 yuan/ton (cash).

5. Medium-to-high sulfur calcined petroleum coke (3.5% sulfur, no requirement for trace elements): Previous ex-factory mainstream contract prices were 2,350–2,450 yuan/ton (cash); current negotiated prices are the same.

6. Medium-to-high sulfur calcined petroleum coke (3.0% sulfur, vanadium 400): Previous contract prices were 3,500–3,700 yuan/ton (cash); currently negotiated ex-factory prices remain at 3,500–3,700 yuan/ton (cash).

Supply Side

Currently, China's commercial calcined petroleum coke daily supply is 27,693 tons, with an operating rate of 59.69%. Compared with the previous working day, calcined petroleum coke market supply has increased by 0.32%.

Upstream Market

Petroleum Coke: At present, Sinopec-affiliated refineries are delivering as needed, with some prices slightly increasing since April 7. In the Yangtze River region, anode coke prices generally increased by 50 yuan/ton, and carbon coke increased by 30–80 yuan/ton. In East China, some increased by 50 yuan/ton. In North China, Yanshan Petrochemical has depleted its inventory of 4B and No.5 coke and stopped quoting; currently producing No.3 coke. Other refineries raised prices by 20–50 yuan/ton. In Shandong, Qilu Petrochemical maintained stable prices, while other refineries raised prices by 30–80 yuan/ton. In South China, Guangzhou Petrochemical raised prices by 20–50 yuan/ton for some grades.

PetroChina-affiliated refineries mainly ship at stable prices. Northeast refineries are expected to see increased maintenance, and supply-side factors provide short-term price support. In the Northwest, supply and demand remain stable, and prices are temporarily unchanged. CNOOC-affiliated refineries are conducting normal auctions, and final prices have not yet been announced—please continue to follow Baichuan Yingfu.

Downstream Market

Graphite Electrode: Trade frictions and tariff disputes are intensifying internationally, and the graphite electrode export situation is tense. Domestic enterprises have rising panic sentiment. Meanwhile, low-price resources are active in the domestic market, hitting bottom-line prices. Mainstream transaction focus is unstable with a trend of hidden discounts. Downstream buyers are mostly observing the market and being cautious in procurement. The graphite electrode market is running weak and stable overall.

Aluminum (Electrolytic Aluminum): External markets continue to exert pressure, and in the context of international tariff confrontations, the market holds a bearish view on aluminum prices in the short term. Spot transactions are weak, and spot aluminum prices are declining.

Anode Materials: The anode materials market remains stable for now, but oversupply continues. Low- and mid-end anode materials suffer from severe product homogenization. As a result, battery cell factories focus heavily on price comparisons and bargaining during procurement, maintaining a price-suppressing mindset. Anode material prices continue at low levels.

Market Outlook

Demand for low-sulfur calcined petroleum coke remains weak, and prices are expected to remain stable. Medium-to-high sulfur calcined petroleum coke prices are overall stable, with slight fluctuations in some grades depending on market conditions.

(Source: Baiinfo)

Feel free to contact us anytime for more information about the calcined petroleum coke market. Our team is dedicated to providing you with in-depth insights and customized assistance based on your needs. Whether you have questions about product specifications, market trends, or pricing, we are here to help.

Procurement Context

Use archive content as a starting point for specification review

For current orders, please confirm product name, target specifications, quantity, packing, destination and application. Final quotation depends on available batch and order confirmation.