This page is part of the English restoration corpus. It keeps noindex during review and does not replace existing high-ID archive shells.

Graphitized petroleum coke recarburizer features high fixed carbon, low sulfur, and high absorption rate. It effectively increases carbon content and improves product quality, widely used in steelmaking, casting, and carbon industries.

【Petroleum Coke】Upstream and Downstream Market Dynamics Keep Coke Prices in Narrow Fluctuation

In May, crude oil prices remained at elevated levels, pushing refinery costs higher and narrowing coking margins. Increased refinery maintenance led to a reduction in domestic supply. However, imported petroleum coke resources increased year-on-year, while port inventories remained above 3.8 million tons, indicating no significant short-term supply pressure. On the demand side, purchasing activity slowed, causing prices of some petroleum coke grades to decline. It is expected that in June, operating rates of domestic delayed coking units will continue to decline slightly, domestic resource supply will tighten further, imported petroleum coke arrivals will decrease, and overall market supply will continue to contract.

I. Domestic Petroleum Coke Supply Remains Adequate

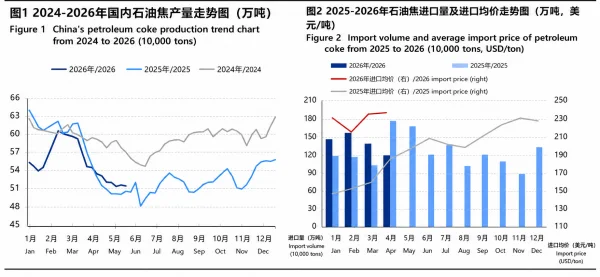

From January to May, China's petroleum coke production is estimated at 11.90 million tons, down 417,000 tons year-on-year, a decrease of 3.39%. Production in May is estimated at 2.2482 million tons, down 17,600 tons month-on-month.

Regarding imported petroleum coke, China's imports of uncalcined petroleum coke reached 1.2437 million tons in April, down 178,700 tons from March, a decline of 12.36%, and down 579,400 tons year-on-year, a decrease of 31.78%. The average import price of petroleum coke was USD 244.62/ton, up USD 1.77/ton month-on-month, an increase of 0.73%.

Among all suppliers, the United States remained the largest source, exporting 481,600 tons to China at an average import price of USD 180.59/ton. Cumulative imports from January to April totaled 5.7561 million tons, an increase of 413,700 tons year-on-year, up 17.28%.

Overall, although domestic petroleum coke supply declined slightly, imported resources increased significantly year-on-year, and total market supply remained relatively sufficient.

II. Petroleum Coke Prices Mainly Declined in May but Remained High Year-on-Year

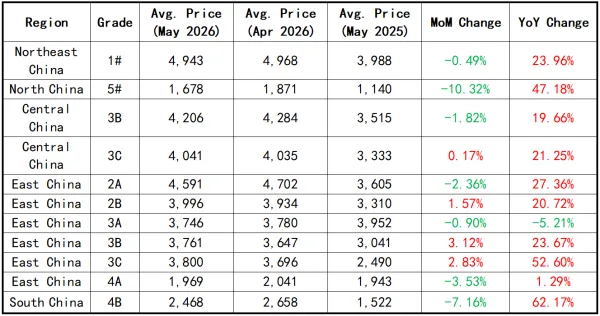

Average Price Comparison by Region and Grade (May 2026)

Unit: RMB/ton

From a pricing perspective, the domestic petroleum coke market mainly trended downward during May.

Among major state-owned refineries, downstream anode material producers faced difficulty passing on cost pressures, limiting their acceptance of high-priced feedstock. Combined with increased maintenance among graphite electrode producers and environmental inspections in Northeast China, shipments of low-sulfur coke in the region slowed, resulting in price declines.

Sinopec refineries adjusted prices within a narrow range throughout the month. Shipments of petroleum coke used for battery anode materials were relatively average, leading some refineries to reduce prices by a cumulative RMB 40–320/ton.

Meanwhile, due to crude oil shortages affecting Sinopec operations, more refineries entered maintenance, reducing output. Petroleum coke suitable for prebaked anodes experienced cumulative price increases of RMB 50–200/ton.

As the supply of high-sulfur commodity grades increased, prices of Grade 4# and Grade 5# petroleum coke declined by RMB 100–270/ton during the month.

CNOOC Taizhou Petrochemical and Zhoushan Petrochemical remained under maintenance throughout the month, with inventories largely sold out. Low-sulfur petroleum coke prices at CNOOC Binzhou were supported by reduced supply and remained stable, while Huizhou Refinery mainly fulfilled long-term contract orders.

Prices at independent refineries fluctuated, with downstream enterprises purchasing opportunistically at lower prices. Overall transaction prices remained at relatively high levels.

III. Stable Port Clearance of Imported Coke, Spot Inventories Continue to Decline

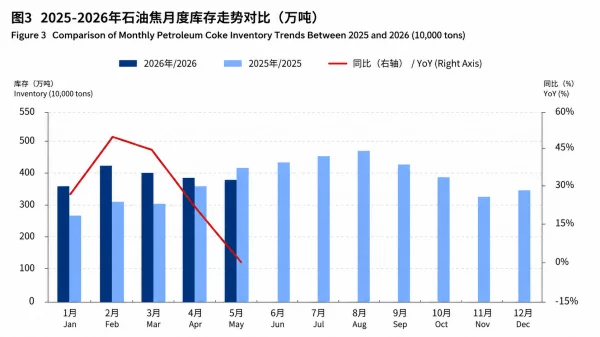

Figure 3. Comparison of Monthly Petroleum Coke Inventory Trends (2025–2026)

In May, total spot petroleum coke inventories at domestic ports stood at 3.8122 million tons, down 84,000 tons month-on-month, a decrease of 2.16%, and down 401,500 tons year-on-year, a decline of 9.53%.

During the month, total port inflows of petroleum coke were lower than outflows. Arrivals of imported petroleum coke decreased, while downstream users maintained demand-driven procurement. Some traders actively secured orders to promote shipments.

As a result, imported petroleum coke continued to move steadily through ports, and spot inventories maintained a downward trend.

On the demand side, market participants replenished inventories cautiously based on production needs. Support from domestic petroleum coke varied among grades. Monthly spot transaction prices at ports showed mixed performance, with medium-sulfur shot coke priced at approximately RMB 2,300/ton, while medium-to-high sulfur sponge coke fluctuated around RMB 1,930/ton.

IV. Increased Refinery Maintenance in May Reduced Supply

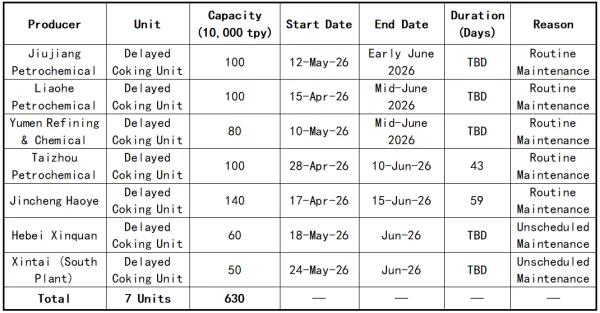

Delayed Coking Unit Maintenance Schedule (2026)

In June, many refineries that entered maintenance earlier are expected to remain offline. Maintenance activities currently involve delayed coking capacity totaling 30.8 million tons per year.

At the same time, delayed coking units with a combined annual capacity of 6.3 million tons at the following facilities are scheduled to resume operations:

·Jiujiang Petrochemical

·Liaohe Petrochemical

·Yumen Refining & Chemical

·Taizhou Petrochemical

·Panjin Haoye

·Hebei Xinquan

·Xintai Petrochemical South Plant

Petroleum coke production is expected to decline further next month, which may provide certain support for petroleum coke prices.

In the short term, the anode material sector remains cautious and purchases mainly on a demand-driven basis, creating shipment pressure for high-priced feedstock. Traditional carbon material producers continue procurement according to production requirements.

With the arrival of the wet season, operating rates at primary aluminum smelters continue to increase. Purchasing inquiries from the silicon metal industry are also becoming more active, providing stable support for petroleum coke shipments.

Coupled with expectations for lower operating rates at domestic delayed coking units, petroleum coke prices are expected to remain generally stable while fluctuating within a narrow range.

Feel free to contact us anytime for more information about the petroleum coke market. Our team is dedicated to providing you with in-depth insights and customized assistance based on your needs. Whether you have questions about product specifications, market trends, or pricing, we are here to help.

Procurement Context

Use archive content as a starting point for specification review

For current orders, please confirm product name, target specifications, quantity, packing, destination and application. Final quotation depends on available batch and order confirmation.