This page is part of the English restoration corpus. It keeps noindex during review and does not replace existing high-ID archive shells.

Graphite electrodes are the essential consumables in EAF steelmaking. Due to their outstanding electrical conductivity and excellent high-temperature resistance, they play a critical role in ensuring efficient and stable furnace operation, thereby improving steel production capacity and product quality.

【Steel Industry】Manufacturing Now Accounts for Half of Demand, Reshaping the Logic of Steel Consumption in 2026

Demand Transformation

Manufacturing Support Creates New Structural Opportunities

Moderate Recovery in Domestic Demand: Infrastructure Provides Support, Manufacturing Becomes the Backbone, and Structural Transformation Continues.

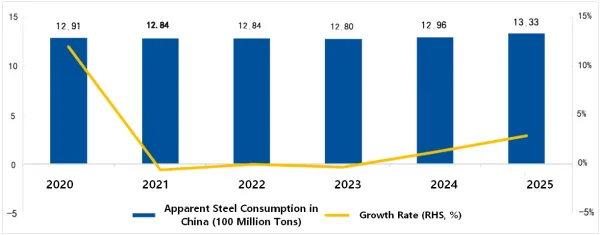

In recent years, China's steel market has been undergoing a transformation in demand structure. Manufacturing demand now accounts for approximately half of total steel consumption, surpassing the real estate sector as the largest consumer of steel products.

In 2025, the floor area of newly started real estate projects continued to decline by 20.4% year-on-year, although the rate of decline narrowed slightly. Land transaction volumes in 2025 remained near five-year lows, suggesting that new housing starts in 2026 are unlikely to improve significantly.

Manufacturing has become the primary driver of steel demand restructuring. Demand for steel from high-end manufacturing industries continues to increase, although investment growth slowed somewhat in 2025. Among specific sectors, the automotive and shipbuilding industries maintained strong momentum, the machinery sector continued to expand steadily, and the power equipment and high-tech equipment sectors remained on a growth trajectory.

The real estate industry is expected to remain in a bottoming phase throughout 2026. The impact of new construction on steel demand is gradually shifting toward the influence of existing housing stock, while the pace of decline is expected to continue narrowing. As 2026 marks the opening year of China's 15th Five-Year Plan, major infrastructure projects are expected to gradually enter the implementation stage, providing support for infrastructure investment. Although manufacturing demand growth has slowed, it remains one of the most important pillars supporting steel consumption.

Slower Export Growth: Entering an Era of High-Quality Transformation Amid New Policy Challenges

In recent years, steel exports have served as a valuable supplement to steel demand. However, affected by trade frictions, export growth slowed in 2025. Direct steel exports increased by 7.5% year-on-year.

Regarding indirect exports, exports of mechanical and electrical products and ships increased by 8.4% and 26.70%, respectively, although ship export growth slowed compared with previous years.

Overall, China's steel exports are expected to enter an era of high-quality transformation in 2026. Effective January 1, 2026, China implemented export licensing requirements for steel products under 300 customs commodity codes. Industry participants have also called for the restoration of export tax rebates for high-end steel products, alongside stricter quality control measures, guiding enterprises to shift from a "volume-over-price" strategy toward high-quality development.

It is expected that China's steel exports will remain at a substantial scale in 2026, while the export product structure continues to improve.

Demand Opportunities: Structural Reconfiguration Creates New Regional and Industrial Growth Drivers

According to forecasts by the World Steel Association, global steel demand is expected to increase by 1.3% year-on-year in 2026.

Although steel demand remains in a bottom-recovery phase, the industry is facing significant opportunities arising from structural reconfiguration.

Affordable housing projects are becoming an important driver of new housing development. Urban redevelopment projects, old residential community upgrades, and age-friendly community construction are gradually replacing traditional large-scale expansion projects.

Supported by policies such as ultra-long-term special government bonds, infrastructure investment is expected to maintain positive growth.

Manufacturing upgrades, together with consumer stimulus policies for automobiles and home appliances, are expected to sustain rigid demand for steel products. Investment in manufacturing—particularly in high-tech industries and equipment manufacturing—is expected to maintain relatively strong growth.

From a regional perspective, major projects in Southwest China, including the Sichuan-Tibet Railway, the Yarlung Zangbo River Project, and the Yinda-Jimin Water Diversion Project, are expected to increase steel demand significantly.

In addition, exports still account for approximately 70% of global steel consumption. Emerging markets and recovering economies in Europe and North America are expected to generate new demand momentum.

Supply Transformation

Moving Toward a New Pattern of Reduced Output, Green Development, and High-Quality Growth

Supply-Demand Mismatch: Differentiated Production Controls and Voluntary Output Cuts Improve Market Balance

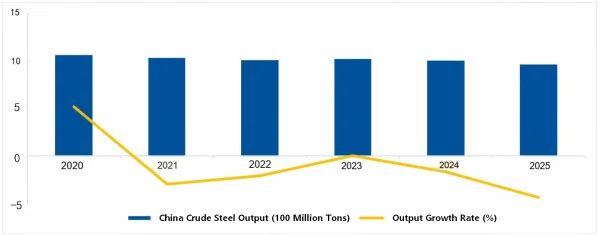

In 2021, in response to China's "Dual Carbon" strategy, the government proposed for the first time that crude steel output should not increase year-on-year. Since then, annual crude steel production has been subject to output-control policies.

During 2025–2026, China continued implementing precise production-capacity and output regulation measures. Production reduction policies remain in place under the principle of supporting advanced enterprises while accelerating the exit of outdated and inefficient capacity.

Annual production control targets are designed to promote dynamic supply-demand balance.

At the same time, considering demand conditions and profitability levels, some steel enterprises have voluntarily reduced production. As a result, China's crude steel output reached another low point in 2025, although finished steel production still recorded slight growth.

Crude steel capacity is expected to continue declining gradually in 2026. The industry will further address supply-demand mismatches and focus on optimizing product structures in areas such as high-end equipment manufacturing and core industrial components.

Supply Structure: Advancing Toward Green and High-Quality Development

Historically, China's steel capacity distribution has been characterized by a strong concentration in northern regions, while consumption has been concentrated in southern markets, resulting in long transportation distances.

To address this imbalance, China has gradually shifted production capacity toward coastal and southern regions through capacity replacement programs and market competition mechanisms. Northern regions are transitioning from traditional production centers toward technology-focused development, forming a pattern characterized by:

· High-end steel production along the eastern coast

· Resource-based steel production in western inland regions

The steel industry is also expected to continue consolidation and restructuring efforts to improve industry concentration and achieve complementary advantages among enterprises.

Northeast China remains an important northern industrial hub with strong technological capabilities and well-developed industrial support systems. However, production capacity has declined, and the region is expected to transition from a major production base into a resource-processing hub and supplier of advanced steel materials.

Eastern coastal regions are expected to become the primary drivers of industry development due to their large-scale capacity, advanced technologies, proximity to ports, and efficient logistics networks. However, higher industry concentration also results in more intense market competition.

Central China serves as an important supplement to national steel capacity. The region benefits from a solid industrial foundation, proximity to coal-producing areas, and strategic transportation advantages.

Western China primarily competes within regional markets due to longer transportation distances. Supported by local resources and favorable policies, the region is increasingly undertaking industrial transfers from eastern China and developing specialized steel industries.

Green and Intelligent Transformation

From an Optional Strategy to a Mandatory Requirement, From Fragmented Efforts to Systematic Development

Fundamental Transformation: Carbon Reduction Progress Emerges as Technology Drives Innovation

In recent years, China's steel industry has introduced a series of policies to standardize green and digital development.

In 2021, China released the Action Plan for Carbon Peaking Before 2030, identifying the steel industry as one of the ten key sectors in the national carbon-peaking strategy. This marked the beginning of a new era in which steel production became increasingly linked to carbon emissions and energy efficiency performance.

In 2022, the Guiding Opinions on Promoting High-Quality Development of the Steel Industry proposed that more than 80% of steelmaking capacity should complete ultra-low-emission upgrades by 2025.

In 2024, the 2024–2025 Energy Conservation and Carbon Reduction Action Plan established targets for comprehensive energy consumption per ton of steel and self-generation rates from waste heat, waste pressure, and residual energy recovery.

In 2025, the Work Plan for Expanding China's National Carbon Emissions Trading Market to the Steel, Cement, and Aluminum Smelting Industries preliminarily defined the rules for incorporating the steel industry into the national carbon trading system.

Since the launch of the "Dual Carbon" initiative, China's steel industry has accelerated its transformation.

By the end of 2025, approximately 844 million tons of crude steel capacity had completed ultra-low-emission upgrades and evaluation monitoring, accounting for nearly 80% of national capacity.

Compared with the end of the 13th Five-Year Plan period, emissions concentrations of particulate matter, sulfur dioxide, and nitrogen oxides had declined by approximately 50% by the end of 2025.

China's first one-million-ton near-zero-carbon steel production line was successfully commissioned at Baosteel Zhanjiang Steel, marking a major milestone in the industrial application of hydrogen metallurgy technology and placing China among the global leaders in low-carbon steelmaking innovation.

Feel free to contact us anytime for more information about the EAF Steel market. Our team is dedicated to providing you with in-depth insights and customized assistance based on your needs. Whether you have questions about product specifications, market trends, or pricing, we are here to help.

Procurement Context

Use archive content as a starting point for specification review

For current orders, please confirm product name, target specifications, quantity, packing, destination and application. Final quotation depends on available batch and order confirmation.