This page is part of the English restoration corpus. It keeps noindex during review and does not replace existing high-ID archive shells.

Graphite electrodes are the essential consumables in EAF steelmaking. Due to their outstanding electrical conductivity and excellent high-temperature resistance, they play a critical role in ensuring efficient and stable furnace operation, thereby improving steel production capacity and product quality.

【Steel Industry】Accelerating Digitalization and Profit Recovery—Where Is the Industry Heading in 2026?

In December 2023, the Ministry of Industry and Information Technology (MIIT), together with the National Development and Reform Commission (NDRC) and seven other government departments, jointly issued the Digital Transformation Action Plan for the Raw Materials Industry (2024–2026). Alongside the plan, the Implementation Guidelines for Digital Transformation in the Steel Industry were released, further defining the key objectives of digital transformation from three dimensions: strengthening digital infrastructure, significantly enhancing digital empowerment, and increasing demonstration effects.

The plan aims to significantly improve the overall digitalization level of China's steel industry by 2026, promote the deep integration of next-generation information technologies with steel manufacturing, continuously improve the industry's digital ecosystem, and fundamentally shift the industry from isolated and localized digital applications toward systematic and comprehensive digital development.

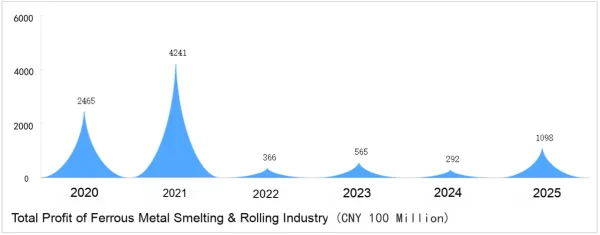

Profit Recovery

Winning the Turnaround Through Better Economics

Profit Recovery: Lower Raw Material Costs and Anti-Overcapacity Measures Raise the Price Floor for Steel

In 2025, the total profit of China's steel industry recorded its strongest recovery since 2022, increasing by more than 270% year-on-year.

On one hand, average prices of iron, coke, and iron ore all declined to varying degrees. Coke prices experienced the largest decline, followed by coal prices, both of which fell more than average steel prices. Iron ore prices showed the smallest decline and remained relatively resilient.

As a result, the steel industry witnessed a significant improvement in gross profit margins compared with the previous two years.

On the other hand, the China Iron and Steel Association (CISA) promoted the principles of "Three Determinations and Three Don'ts" and "Self-Disciplined Production Control and Inventory Reduction." These initiatives continued to encourage industry-wide output reduction and structural optimization, enabling steel enterprises to achieve production based on actual demand, profitable manufacturing, and sales with reliable cash collection.

Under the expected weak supply and weak demand environment in 2026, profit recovery will still depend heavily on the strict implementation of production controls. Iron ore supply is expected to remain relatively abundant, while coal and coke markets may continue to offer cost concessions. Consequently, profitability in the steel industry is expected to maintain a modest recovery trend.

Profit Support: Every Enterprise Has Its Own Strategy, but Technology Remains the Key to a Turnaround

In 2025, more than 80% of steel enterprises (listed companies or bond issuers) achieved growth in net profit, while nearly 50% reported positive earnings.

Overall, the improvement was mainly driven by higher gross profits, reflecting the recovery of profitability in core steelmaking operations.

The recovery in core business profitability resulted partly from lower raw material costs and partly from the benefits of structural transformation and optimization implemented in recent years.

In addition, during the industry's downturn, major steel producers placed greater emphasis on cost reduction and efficiency improvement through refined cost-control measures.

Credit Stability

Stable Credit Quality and Narrowing Yield Spreads

Debt Servicing Performance: Profit Recovery and Reduced Investment Pressure Support Solvency

Production control policies are expected to continue throughout 2026. Demand is unlikely to provide strong support for steel prices, which are expected to fluctuate within a limited range.

Total revenue of steel enterprises is expected to remain stable, while revenue quality improves.

In terms of profitability, major raw material and fuel supplies are expected to remain relatively ample. Raw material price resilience is weakening, and steel producers continue to advance product structure transformation, increasing the proportion of higher-margin products. As a result, gross profit margins in core operations are expected to maintain their recovery trend.

By 2026, most investments in ultra-low-emission retrofits by major steel enterprises are expected to be largely completed. Future investments will focus primarily on product upgrades and green-intelligent transformation.

However, interest expenses on outstanding debt remain substantial, and free cash flow coverage of debt obligations remains limited.

Therefore, debt-servicing pressure is expected to persist in 2026, although solvency should improve slightly. Companies with superior product structures, lower future capital expenditure requirements, reduced financing costs, and lighter historical debt burdens are expected to demonstrate stronger debt repayment capabilities.

Bond Market Performance: Yield Spreads Continue to Narrow While Financing Activity Remains Active

In 2025, approximately RMB 180 billion worth of new bonds were issued by the steel industry, involving more than 20 issuing entities.

Both total issuance volume and the number of issuers remained relatively stable, while net financing increased significantly year-on-year. Issuers continued to be primarily local state-owned enterprises and central government-owned enterprises.

Steel industry bond spreads remained among the highest within upstream and midstream industrial sectors in 2025, although the gap narrowed further, with most steel companies achieving lower credit spreads.

It is expected that new bond issuance in 2026 will continue to be dominated by high-credit-quality issuers. Major steel enterprises will still require debt refinancing, while ongoing production line upgrades will sustain a considerable level of bond issuance and outstanding debt.

Moving Toward the Future

From "Scale Expansion" to "Higher Quality and Sustainable Growth"

During the 14th Five-Year Plan period, China's steel industry policy framework evolved from fragmented responses to systematic strategic planning, and from end-of-pipe governance toward comprehensive restructuring at the source.

Policy documents such as the Work Plan for Stabilizing Growth in the Steel Industry (2025–2026) and the Steel Industry Regulatory Conditions (2025 Edition) have clearly reaffirmed that maintaining stable growth remains the central policy objective in 2026, while the industry continues advancing toward output reduction and quality improvement.

Overall, steel demand in 2026 is expected to remain in a period of structural adjustment and gradual recovery from the bottom of the cycle, although significant structural opportunities are emerging.

On the supply side, steel enterprises will continue to exercise self-discipline in production control, accelerate the replacement of conventional products with higher-end alternatives, and maintain reasonable profitability.

Green and intelligent transformation has evolved from a strategic option into a fundamental requirement for survival. Through improvements in environmental performance, digitalization, and intelligent manufacturing, steel enterprises will be better positioned to achieve compliant, efficient, and sustainable development.

Feel free to contact us anytime for more information about the EAF Steel market. Our team is dedicated to providing you with in-depth insights and customized assistance based on your needs. Whether you have questions about product specifications, market trends, or pricing, we are here to help.

Procurement Context

Use archive content as a starting point for specification review

For current orders, please confirm product name, target specifications, quantity, packing, destination and application. Final quotation depends on available batch and order confirmation.