This page is part of the English restoration corpus. It keeps noindex during review and does not replace existing high-ID archive shells.

Graphitized petroleum coke recarburizer features high fixed carbon, low sulfur, and high absorption rate. It effectively increases carbon content and improves product quality, widely used in steelmaking, casting, and carbon industries.

【Petroleum Coke】May Prices Ended on a Volatile Note – Which Factors Will Shape the June Market?

Petroleum Coke Market Analysis

Overall Market Overview for May:

The domestic petroleum coke market generally remained weak in May, with prices declining across most grades and overall trading activity remaining moderate. From a broad perspective, the average petroleum coke price decreased month-on-month. Total supply contracted due to increased refinery maintenance and lower import volumes, while overall demand remained subdued as downstream operating rates declined. Meanwhile, port inventories continued to decrease.

Low-sulfur petroleum coke experienced a notable price decline due to environmental inspections in Northeast China and adjustments to sales policies. Medium-sulfur petroleum coke saw slower shipment volumes and lower average prices. High-sulfur petroleum coke was the most affected by weak market sentiment, recording the largest decline among all grades. Regionally, prices in major markets including Northeast China, East China, and South China all fell to varying degrees. Internationally, arrivals from major supplying countries decreased due to geopolitical factors, while freight rates remained elevated.

On the supply side, domestic petroleum coke production declined slightly month-on-month. The average operating rate of delayed coking units fell, with both state-owned refineries and independent refineries reporting lower operating levels. A relatively large number of units underwent maintenance, resulting in a significant increase in maintenance-related production losses. Import volumes also declined month-on-month, although the structure of major source countries remained largely unchanged. Port inventories continued to be destocked, with reduced inbound cargoes and stable port shipments.

On the demand side, operating rates across most downstream sectors declined. The prebaked anode sector remained relatively stable, while operating rates in the anode material sector dropped significantly. Graphite electrode and recarburizer production also weakened. In terms of purchasing behavior, downstream enterprises generally maintained a cautious attitude, purchasing mainly to meet immediate production needs and showing limited acceptance of high-priced raw materials.

Market Outlook

Looking ahead to June, the petroleum coke market is expected to maintain a stable yet fluctuating trend, with prices largely stable but subject to minor adjustments and transaction levels potentially edging lower. Low-sulfur petroleum coke is expected to remain range-bound due to downstream cost pressures and maintenance activities in the graphite electrode sector, limiting upside potential. Medium-sulfur petroleum coke prices may fluctuate more flexibly as its market share continues to increase. High-sulfur petroleum coke faces relatively weak demand support and bearish market sentiment, making a significant rebound unlikely.

Overall, supply-demand imbalances are expected to persist in June. While prices may find support near current levels, cautious downstream purchasing sentiment is likely to limit upward momentum. Market participants are advised to closely monitor refinery profitability, the pace of port inventory reductions, and the realization of demand during the wet-season production period.

From the supply perspective, most refineries that entered maintenance earlier are expected to remain offline. Although some units are scheduled to restart, overall operating rates are likely to remain low, leading to continued tightening of domestic petroleum coke supply. Import arrivals are also expected to decline further. Combined with ongoing inventory drawdowns at ports, the availability of spot cargoes may become increasingly tight.

On the demand side, prebaked anode operating rates are expected to remain stable, while procurement by anode material producers is likely to remain cautious. However, as the wet season begins in June, operating rates at downstream aluminum smelters and silicon producers are expected to increase, providing some support for petroleum coke consumption and shipments.

Regarding costs, feedstock residue oil prices are expected to soften, which may ease cost pressures on delayed coking operations. Market participants should also pay close attention to the impact of geopolitical developments on import logistics, as well as potential disruptions to production caused by domestic environmental protection policies in certain regions.

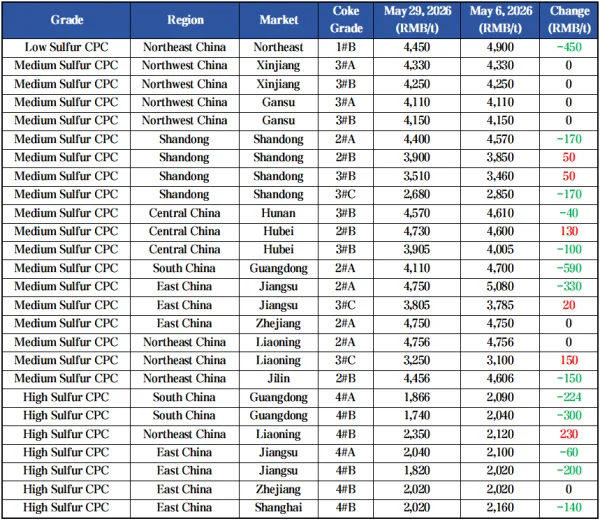

Monthly Petroleum Coke Price Trend Comparison

Unit:RMB/Ton

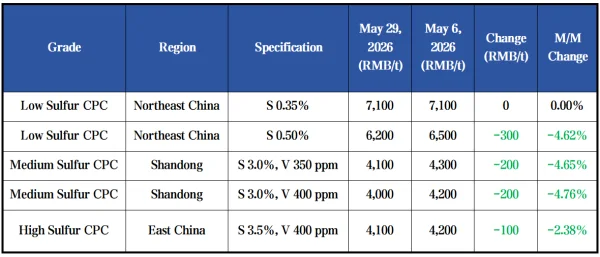

Monthly Calcined Petroleum Coke (CPC) Price Trend Comparison

Unit:RMB/Ton

Feel free to contact us anytime for more information about the petroleum coke market. Our team is dedicated to providing you with in-depth insights and customized assistance based on your needs. Whether you have questions about product specifications, market trends, or pricing, we are here to help.

Procurement Context

Use archive content as a starting point for specification review

For current orders, please confirm product name, target specifications, quantity, packing, destination and application. Final quotation depends on available batch and order confirmation.